Financial Resilience 2026: Practical Money Resilience Habits for Americans

November 20, 2025 · admin · Finance

Introduction: A New Era of Practical Money Resilience in the U.S.

If you’re searching for practical money resilience habits for Americans, you are part of a growing national shift. Across the United States, households are facing a financial environment unlike anything seen in the past decade: rising prices, higher interest rates, unpredictable job markets, and a lingering sense of economic instability. Financial resilience has moved from being a “good idea” to a necessary survival skill.

In 2026, Americans can no longer rely on outdated budgeting methods or temporary fixes. They need financial habits that are flexible, sustainable, and grounded in real-world behavior — not rigid systems that collapse under stress. That’s where practical money resilience habits for Americans come in. These habits blend intentional spending, emotional awareness, adaptive planning, and long-term security into daily routines that support stability in a fast-changing world.

This guide will help you build resilience not through drastic changes, but through small, repeatable actions that strengthen your financial life week by week. By the end of this three-part series, you will have a blueprint for weathering uncertainty, thriving through change, and building a financial foundation you can trust.

Why Financial Resilience Matters Right Now in the U.S.

Before we dive into the practical money resilience habits for Americans, we need to understand why resilience is so essential in 2026.

Here are the financial realities shaping American households:

1. Rising Cost of Living

Grocery prices, rent, utilities, and fuel remain higher than pre-2020 levels. Even small fluctuations create strain for millions.

2. Persistent Consumer Debt

Credit card balances are at their highest point in U.S. history. Interest rates continue to rise. Minimum payments eat into household budgets.

3. Job Market Uncertainty

Automation, hybrid workflows, layoffs in certain industries, and gig-economy volatility all influence income security.

4. Inflation Fatigue

Even when inflation slows, prices rarely return to previous levels—meaning Americans must adapt to “new normal” spending.

5. Low Savings Reserves

According to recent surveys, many households have less than $500 saved. This intensifies the need for resilience habits that rebuild security slowly but consistently.

6. Emotional Financial Burnout

Money stress impacts sleep, mental health, and relationships. Americans need calm, repeatable habits—not anxiety-driven urgency.

This environment demands more than budgeting. It requires resilience — a skillset built from practical, mindful, everyday habits.

The Psychology of Financial Resilience

Financial resilience is not just about numbers. It is deeply psychological.

Here are the mindset shifts that make resilience powerful:

1. Awareness Over Avoidance

Many Americans cope with financial stress by avoiding:

-

checking bank accounts

-

opening bills

-

reviewing card statements

-

acknowledging debt balances

Resilience begins with honesty.

Awareness is not punishment — it is empowerment.

2. Planning Instead of Panicking

Panicked decisions lead to:

-

impulse spending

-

emotional purchases

-

high-interest debt

-

poor long-term planning

Resilience replaces panic with calm, pre-decided solutions.

3. Flexibility Instead of Perfection

Rigid budgets break easily.

Flexible habits survive change.

Financial resilience thrives when you allow:

-

adjustments

-

category shifts

-

life changes

-

seasonal differences

This mindset is essential for practical money resilience habits for Americans.

4. Prevention Instead of Reaction

Resilience builds buffers before emergencies happen.

This reduces emotional and financial shock.

5. Small Wins Over Huge Leaps

Tiny, repeatable habits create massive resilience.

Examples:

-

saving $3 a day

-

rounding up purchases

-

reviewing subscriptions monthly

-

preparing one extra meal at home

-

adding $10 weekly to emergency savings

Small equals sustainable.

The Resilience Ladder: The Foundation of American Financial Stability

Before introducing the core habits, we must define the resilience ladder — a staged system that helps Americans build stability step by step.

Think of it as the financial equivalent of climbing stairs instead of trying to jump to the top.

Stage 1 — Clarity

Know your numbers:

-

monthly essentials

-

minimum debt payments

-

subscription list

-

total income

-

upcoming bills

Clarity removes fear.

Stage 2 — Micro-Buffer (Mini Safety Net)

Start with $50.

Then $100.

Then $250.

This helps absorb tiny financial shocks.

Stage 3 — Baseline Emergency Fund ($1,000)

This is not perfection — it is the minimum resilience needed to stay afloat during sudden events.

Stage 4 — One Month of Expenses

This is where Americans begin feeling true flexibility.

Stage 5 — Three Months of Expenses

Long-term, realistic resilience for the average household.

Foundational Practical Money Resilience Habits for Americans

These habits form the base of everything else.

They are simple, low-effort, and extremely high impact.

1. The Daily Account Awareness Habit (30–60 Seconds)

Check your accounts once a day — gently, not obsessively.

This builds:

-

emotional confidence

-

awareness

-

spending control

-

unconscious accountability

Even if you check and change nothing, the habit builds resilience.

2. The $5–10 Daily Micro-Saving Technique

American households underestimate the power of small savings.

Examples:

-

$7/day becomes $210/month

-

$10/day becomes $300/month

-

$5/day becomes $150/month

Money resilience is built from micro-habits, not massive leaps.

You can automate small transfers daily or weekly.

3. The 24-Hour Rule for Purchases

A foundational habit that reduces impulse spending:

“If it’s not essential, wait 24 hours before buying.”

This helps Americans avoid:

-

Amazon impulse buys

-

late-night spending

-

emotional shopping

-

Deal-of-the-day traps

This rule alone can save $200–$400 per month.

4. The “Checklist Before Checkout” Pause

Before purchasing anything, use this mindful checklist:

-

Do I need this?

-

Do I want this?

-

Will this matter next week?

-

Does this support my resilience goals?

-

Am I reacting to stress?

-

Did I plan for this?

This slows emotional purchasing and builds long-term resilience.

5. Build Your “Resilience Categories” in Your Budget

Your budget should include at least these categories:

✔ Emergency Fund

✔ High-priority sinking funds

✔ Groceries (with a weekly ceiling)

✔ Utilities

✔ Healthcare

✔ Debt minimums

✔ Transportation

✔ Monthly “flex” buffer

These categories stabilize households even when income or prices change.

6. The Automatic Transfer Rule

Automate:

-

savings

-

emergency fund

-

retirement

-

sinking funds

Automation removes decision fatigue and builds consistency.

7. The Weekly Money Reset (10 Minutes)

Every week:

-

review spending

-

catch errors

-

adjust categories

-

check subscriptions

-

update your plan

A weekly ritual prevents monthly financial disasters.

8. Build a “Financial Calm Corner”

This is a small space (physical or digital) dedicated to:

-

your budget

-

your money plan

-

your savings tracker

-

your spending reflection

Having a calm space strengthens your resilience mindset.

9. Practice the “Needs, Wants, Won’ts” Method

A simple categorization tool:

Needs — essentials

Wants — lifestyle choices

Won’ts — spending areas you intentionally limit

This eliminates guilt and increases clarity.

10. Protect Your Mental Bandwidth

Resilient Americans reduce financial pressure by:

-

lowering the number of bills due

-

consolidating subscriptions

-

using autopay

-

simplifying accounts

-

organizing documents

-

decluttering financial paperwork

Simplicity increases resilience.

In Part 1, you learned the foundational practical money resilience habits for Americans — awareness, micro-savings, mindful spending pauses, automated transfers, and weekly resets. These habits form the base of financial stability.

Now in Part 2, we build on that foundation with:

-

Next-level daily habits

-

Monthly routines

-

Anti-inflation strategies

-

Debt payoff resilience

-

Income stabilization habits

-

Subscription and spending traps

-

Seasonal financial adjustments

-

Real American examples that show how resilience works in daily life

These are the habits that make financial resilience automatic, repeatable, and long-lasting — even during economic uncertainty.

The Advanced Practical Money Resilience System

Below are the extended resilience habits (Steps 11–25+) that help Americans stay financially strong through inflation, price volatility, job shifts, and unexpected expenses.

11. Build a “Resilience Grocery Framework”

Grocery overspending is one of the biggest challenges for American households.

Your goal is not perfection — it’s predictable, intentional grocery spending.

Here’s the mindful resilience system:

✔ Set a weekly grocery ceiling

Weekly ceilings are easier to follow than monthly limits.

✔ Use a simple meal rotation

5–7 repeatable meals you know well.

This eliminates decision fatigue and impulse purchases.

✔ Buy half convenience, half raw ingredients

Realistic for busy American lifestyles.

✔ Never shop hungry or stressed

Two of the top triggers for overspending.

✔ Use a “must use before buying” rule

Check your pantry and freezer before each shopping trip.

This single habit can save Americans $80–$200 per month.

12. Adopt the “48-Hour Rule” for All Non-Essential Online Purchases

The 24-hour pause from Part 1 helps, but the 48-hour rule is your advanced resilience tool.

This eliminates:

-

emotional shopping

-

late-night Amazon buys

-

TikTok and Instagram influencer purchases

-

retail therapy urges

-

algorithm-driven impulse spending

Most desire-based purchases fade when delayed.

This is one of the most powerful practical money resilience habits for Americans.

13. Strengthen Your Financial Boundaries (Not Restrictions)

Boundaries protect your resilience; restrictions destroy it.

Healthy boundaries include:

-

limiting takeout to 1–2 planned nights

-

setting “no spend” windows late at night

-

keeping credit cards out of reach

-

deciding where you will and won’t shop

-

limiting exposure to retail apps

Remember:

Boundaries feel supportive; restrictions feel punishing.

14. Use a Dedicated “Financial Calm Account”

Open a separate savings account just for resilience.

Name it something positive like:

-

Financial Stability Fund

-

Peace Account

-

Resilience Savings

-

Future Security Fund

Labeling accounts is a psychological reinforcement tool.

This is extremely effective for reducing impulsive withdrawals.

15. The “Sinking Fund Trio” Every American Needs

While sinking funds vary by lifestyle, every U.S. household should have three core funds:

✔ Emergency fund

Cushions unexpected disruptions.

✔ Annual expenses fund

For renewals, car registration, insurance premiums, memberships.

✔ Seasonal expenses fund

Covers holidays, travel, school costs, birthdays.

These funds prevent debt, stress, and financial emergencies.

16. Conduct a Monthly “Resilience Audit” (10 Minutes)

At the end of each month, ask:

-

What surprised me financially?

-

What caused stress?

-

What did I handle well?

-

What new habits supported me?

-

Where did I lose money unnecessarily?

-

What will I adjust next month?

A monthly review builds long-term resilience.

17. Build Inflation-Proof Habits (2026 U.S.-Edition)

Inflation in 2026 affects Americans differently depending on region, lifestyle, and income. You need habits that reduce exposure to rising prices.

These include:

✔ Buying in bulk for non-perishables

✔ Using generic brands where possible

✔ Reducing food waste

✔ Tracking unit prices instead of total prices

✔ Adjusting grocery lists monthly

✔ Cooking more at home

✔ Using energy-efficient home habits

✔ Replacing high-cost routines with lower-cost alternatives

Inflation-proofing is a major part of practical money resilience habits for Americans.

18. Build Debt Resilience Using the “5+2 Strategy”

Debt is one of the biggest threats to financial stability.

This strategy creates emotional and financial balance.

✔ Pay all minimums (non-negotiable)

Consistency prevents damage.

✔ Add $5–$20 extra to ONE debt

Momentum matters more than amount.

✔ 2 reflection questions monthly:

-

Which debt hurts the most emotionally?

-

Which debt hurts the most financially?

Alternating between emotional and mathematical priority builds both emotional resilience and financial progress.

19. Build Income Resilience (The “Multiple Streams Mindset”)

Income instability is rising across the U.S., so resilient Americans diversify income sources.

Small, low-effort income streams include:

-

micro freelance tasks

-

selling unused items

-

babysitting or tutoring

-

part-time online services

-

seasonal work

-

YouTube or TikTok informational content

-

Etsy or digital products

-

weekend gig work

Even an extra $50–$100 per week increases resilience dramatically.

20. Master the “Resilience Calendar System”

This is a proactive tool for planning around financial fluctuations.

Your calendar should include:

✔ Subscription renewals

✔ Insurance premium dates

✔ Annual bills

✔ Seasonal expenses

✔ Big life moments

✔ Travel windows

✔ Income cycles

✔ Bill due dates

Visibility creates control and reduces stress.

21. Review Your Financial “Leak Points” Quarterly

Common American leak points include:

-

unused subscriptions

-

late fees

-

overpaying for utilities

-

emotional takeout

-

grocery waste

-

duplicated services

-

unnecessary app purchases

Fixing leak points can save $1,000–$2,500 annually.

22. The “One Big Change per Quarter” Rule

Trying to change too much at once leads to overwhelm.

Resilient Americans focus on one major habit each quarter.

Examples:

-

Quarter 1 → Fix grocery spending

-

Quarter 2 → Reduce debt

-

Quarter 3 → Build savings

-

Quarter 4 → Simplify subscriptions

This approach ensures sustainability.

23. Create a “Spending Identity” Statement

Identity drives action.

Create a sentence like:

-

“I am someone who spends intentionally.”

-

“I am someone who builds resilience daily.”

-

“I spend based on values, not impulses.”

Identity anchors habits deeply.

24. Build the “Financial Peace Cornerstone Habits”

Five cornerstone habits build long-term resilience:

✔ Awareness

✔ Intention

✔ Flexibility

✔ Automation

✔ Reflection

Master these and resilience becomes automatic.

25. Practice Money Mindfulness During High-Stress Moments

Financial resilience is tested most when emotions run high.

In moments of stress:

-

take 5 deep breaths

-

pause before reacting

-

step away from your cart

-

avoid quick fixes

-

remind yourself of your resilience goals

Mindful pausing reduces mistakes that lead to long-term consequences.

U.S. Spending Traps That Undermine Resilience

Understanding these traps strengthens resilience.

1. Algorithm-Driven Shopping

Social media and e-commerce platforms predict desires and push targeted deals.

Resilience response:

The 48-hour rule.

2. Buy Now Pay Later (BNPL)

BNPL creates hidden debt.

Resilience response:

Track BNPL like credit card debt.

3. Seasonal Sales Pressure

Black Friday, July 4th, Labor Day.

Resilience response:

Use sinking funds and pre-planned shopping lists.

4. Convenience Culture Spending

Delivery apps, grocery pickups, subscription passes.

Resilience response:

Choose convenience intentionally, not emotionally.

5. Everyday Micro-Spending

Coffee, snacks, “small” Amazon orders.

Resilience response:

Weekly review + mindful alternatives.

Real-Life American Resilience Scenarios

Here are examples of how resilience habits work in real American households:

Case Study 1 — The Young Professional (Ohio)

Sara struggled with credit card balances and grocery overspending.

After adopting a resilience plan:

-

reduced takeout by $150 monthly

-

added $10/day to savings

-

cut Amazon impulse purchases in half

-

built her first $1,000 emergency fund

Case Study 2 — The Single Dad (Texas)

James faced income instability from gig work.

With resilience habits, he:

-

built a dedicated “gap fund”

-

pre-planned bills by income cycles

-

set a weekly spending limit

-

diversified income with weekend tasks

Case Study 3 — The Family of Four (Georgia)

High grocery spending and surprise school costs caused financial stress.

With resilience tools, they:

-

created sinking funds for school events

-

used meal rotations

-

capped eating out

-

split resilience responsibilities

In Part 1 and Part 2, you explored foundational and advanced practical money resilience habits for Americans — the daily routines, mental frameworks, and spending strategies that anchor financial stability.

In Part 3, we move deeper into:

-

The Seasonal Resilience System Americans need

-

A 12-month resilience routine anyone can follow

-

Mindset tools that keep resilience sustainable

-

The Resilience Response Cycle for unexpected events

-

Annual financial renewal habits

-

U.S.-specific strategies for long-term financial strength

-

Visual placeholders for your article

-

Internal links to strengthen SEO and EEAT

This is where resilience shifts from “daily habit” to lifelong financial security.

The Seasonal Resilience System (Designed for U.S. Households)

Financial resilience requires planning around the rhythms of U.S. life — where expenses rise and fall based on weather, holidays, work cycles, school needs, and national trends.

Below is the four-season resilience structure that helps Americans prevent financial distress long before it appears.

Spring Resilience (March – May)

Spring brings energy, spending spikes, and life transitions.

Financial Themes:

-

Tax season

-

Travel planning

-

Spring break

-

School events

-

Changing utility costs

-

Allergy/medical spending

Spring Resilience Habits:

✔ Plan your tax refund with a 40–30–20–10 Rule

-

40% savings

-

30% debt

-

20% necessities

-

10% intentional joy

✔ Start a summer sinking fund

Vacations, childcare, travel, gas — all unavoidable.

✔ Review subscriptions before summer spending picks up

Delete or pause non-essential services.

✔ Refresh your grocery framework

Seasonal produce lowers grocery costs.

✔ Conduct a spring financial declutter

Digital receipts

Bank app notifications

Expired offers

Paperwork piles

A clean spring mindset supports financial peace.

Summer Resilience (June – August)

Summer is one of the highest-spend seasons in America.

Financial Themes:

-

Vacations

-

Childcare

-

Camps

-

Higher electric bills

-

Barbecues, outings, road trips

-

Back-to-school prep begins early

Summer Resilience Habits:

✔ Complete a “Summer Spending Map”

List all events, travel, and holidays.

✔ Cap last-minute travel expenses

Last-minute decisions are where Americans overspend most.

✔ Use “cooling-off” rules during Prime Day or summer sales

These are the peak impulse-spending events of the year.

✔ Prepare for higher electricity bills

Set aside a seasonal utilities buffer.

✔ Begin back-to-school sinking funds in July

This prevents August financial overwhelm.

Summer can be joyful, but structure protects resilience.

Fall Resilience (September – November)

Fall is the most predictable season — and therefore the best for building savings momentum.

Financial Themes:

-

Back-to-school

-

Sports season

-

Start of holiday spending

-

Upcoming travel

-

Rising grocery demand

Fall Resilience Habits:

✔ Strengthen sinking funds

Holidays

Birthdays

Travel

Year-end bills

✔ Complete a “Pre-Holiday Resilience Review”

This prevents December panic.

✔ Reduce grocery splurges

Fall tends to be food-heavy.

✔ Prepare winter utilities funds

Gas and heating bills rise soon.

✔ Audit subscriptions before holiday sales

Black Friday targets emotional spending.

Fall is the resilience-building season.

Winter Resilience (December – February)

Winter is the emotional and financial pressure point for many Americans.

Financial Themes:

-

Holiday spending

-

Heating bills

-

Travel

-

Post-holiday financial fatigue

-

Annual subscriptions renew

-

New Year motivation

Winter Resilience Habits:

✔ Build a January Recovery Budget

Many Americans overspend in December — recovery must be planned.

✔ Cap gift budgets in early December

Based on income, not emotions.

✔ Reduce exposure to holiday advertising

Limit targeted ads by clearing search history.

✔ Review ALL subscriptions on January 1

January is renewal season for many apps.

✔ Strengthen your emergency fund

Winter weather brings unexpected costs.

Winter resilience protects mental and financial health.

The 12-Month American Resilience Cycle

Below is a simple annual plan that integrates all practical money resilience habits for Americans into a predictable routine.

Quarter 1 — Stabilize

(January–March)

-

Build clarity

-

Start micro-buffer

-

Audit subscriptions

-

Set resilience goals

-

Begin automation

-

Conduct spring planning

Quarter 2 — Strengthen

(April–June)

-

Increase savings

-

Review debt strategies

-

Optimize grocery spending

-

Evaluate summer expenses

-

Advance sinking funds

Quarter 3 — Expand

(July–September)

-

Build income streams

-

Review job skills + career resilience

-

Prepare for fall/winter seasons

-

Reassess spending buckets

-

Protect emergency fund

Quarter 4 — Protect

(October–December)

-

Conduct year-end resilience audit

-

Reduce holiday pressure

-

Refresh financial goals

-

Reduce expenses

-

Plan tax strategies

-

Rebuild January buffer

This cycle keeps American households steady regardless of economic climate.

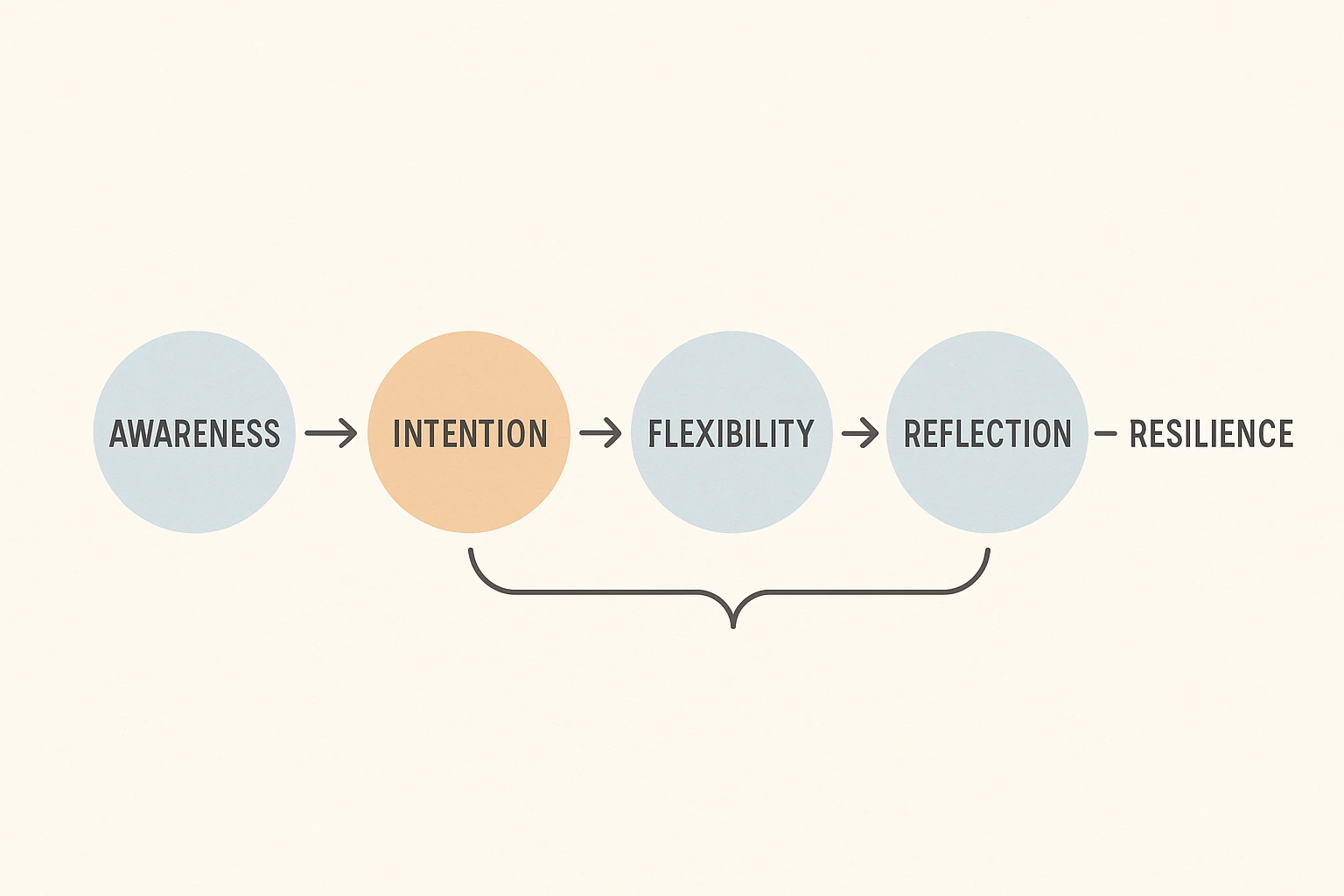

The Financial Resilience Mindset Model

To build long-term practical money resilience habits for Americans, you need a mindset that adapts to reality, not perfection.

Here is the five-part model:

1. Awareness

Know what’s happening with your money.

2. Intention

Make decisions based on values, not momentary impulses.

3. Flexibility

Adjust categories without guilt.

4. Prevention

Build buffers before emergencies appear.

5. Reflection

Review what worked and what didn’t.

This mindset makes resilience a lifestyle.

The Resilience Response Cycle (For Any Financial Shock)

When something unexpected happens — a job loss, emergency bill, car repair, medical cost — follow this simple response cycle:

Step 1: Pause

Avoid panic spending or reaction.

Step 2: Assess the true cost

Not emotional cost — actual cost.

Step 3: Identify resilience tools available

Emergency fund

Sinking funds

Buffer

Cutback categories

Income boosts

Step 4: Reassign money calmly

Shift categories with intention.

Step 5: Update your plan

Small changes = big stability.

Step 6: Reflect and adjust

Every shock teaches you something.

This cycle protects you from emotional decision-making.

Career & Income Resilience for Americans

Financial resilience is not only about spending — it’s about strengthening your earning power.

✔ Learn one new skill per quarter

Digital tools, AI, marketing, software, data literacy.

✔ Keep your résumé and LinkedIn updated

Career resilience is financial resilience.

✔ Build one micro-income stream

Just one.

✔ Track your job industry for large shifts

Awareness reduces shock.

✔ Build networking habits

Relationships create opportunities.

Income resilience multiplies financial resilience.

Money Resilience in Everyday Life (Micro-Examples)

These small habits add up:

-

rotate meals

-

use cash envelopes for emotional categories

-

automate bill reminders

-

clean financial apps weekly

-

keep receipts in a dedicated folder

-

create a “pause basket” for impulse purchases

-

track mini goals, not giant ones

-

use store pick-up instead of free-roaming aisles

-

pack snacks to avoid convenience-store spending

Small equals sustainable.

A simple flowchart highlighting the six habits that build long-term resilience: Awareness, Intention, Flexibility, Prevention, Reflection, and Resilience.

Recommended Suggestions

Conclusion: Financial Resilience Is a Daily Practice, Not a Final Destination

Financial resilience isn’t built overnight.

It’s built through consistency, calm, and clarity — one small habit at a time.

By practicing these practical money resilience habits for Americans, you protect yourself from:

-

inflation swings

-

surprise expenses

-

emotional spending

-

economic uncertainty

-

credit card traps

-

financial fear

Resilience is not perfection.

Resilience is preparation.

And most importantly:

Resilience is confidence — the quiet confidence that you can handle whatever comes next.

Every small action compounds:

Every dollar buffered…

Every expense paused…

Every mindful purchase…

Every plan updated…

This is how Americans build financial stability in 2026.

Not through drastic changes — but through steady, intentional resilience.

You’re not just surviving.

You’re building a financially stronger version of yourself — one mindful habit at a time.

📢 End Note

💬 If this inspired you, share your resilience story with FITHMedia.

🔗 Follow FITHMedia.com on Facebook, X(Twitter), Instagram, Mastodon, Pinterest for weekly financial resets and timeless guides on health, finance, and mindful living.

2 Comments