Emergency Fund USA: Build Your Financial Safety Net

November 21, 2025 · admin · Finance

Emergency Fund USA: Build Your Financial Safety Net

If you’re searching for how to build an emergency fund in the USA or you want a simple, realistic way to create a financial safety net that actually works, you’re in the right place. An emergency fund is the foundation of financial resilience. It keeps everyday Americans from turning every setback into new debt, panic, or missed bills. In this guide, we’ll walk step-by-step through what an emergency fund is, how much you should save, where to keep it, and how to build it even if you feel like you’re starting from zero.

What Is an Emergency Fund (and What It Is Not)?

A Simple Definition

An emergency fund is a dedicated pile of cash set aside only for unexpected, necessary, time-sensitive expenses. It’s your financial safety net, not your “extra spending” account.

You use it when:

-

Something urgent happens

-

It’s truly necessary

-

You didn’t plan for it in your regular budget

Valid emergencies might include:

-

Sudden medical or dental bills

-

Car repairs that keep you from getting to work

-

Job loss or major reduction in hours

-

Essential home repairs (heat, water, electricity, broken fridge)

-

Emergency travel to care for family

Not emergencies:

-

A sale on shoes or electronics

-

Holidays and birthdays you knew were coming

-

Vacations

-

Eating out because you’re tired

-

“I really want this” purchases

Your emergency fund’s job is simple:

Stop life’s surprises from turning into high-interest debt, stress, and chaos.

Why an Emergency Fund Matters So Much in the USA

The U.S. financial system is powerful but unforgiving. Credit cards, Buy Now Pay Later (BNPL), and personal loans are easy to get—and very expensive to lean on in a crisis.

-

Interest rates on credit cards often sit above 22–30%

-

Missed payments hit both your budget and your credit score

-

One emergency can take months or years to fully pay off

An emergency fund acts like a shock absorber for American life:

-

It keeps you from swiping credit when you’re already stressed

-

It gives you time to think before making big decisions

-

It keeps your long-term goals (retirement, investing, home buying) on track

Financial planner “James Holloway, CFP®” often tells clients:

“Your emergency fund is not about being rich. It’s about staying standing when life hits you sideways.”

How Much Should Your Emergency Fund Be?

There is no single perfect number. But there are realistic tiers for Americans at different stages.

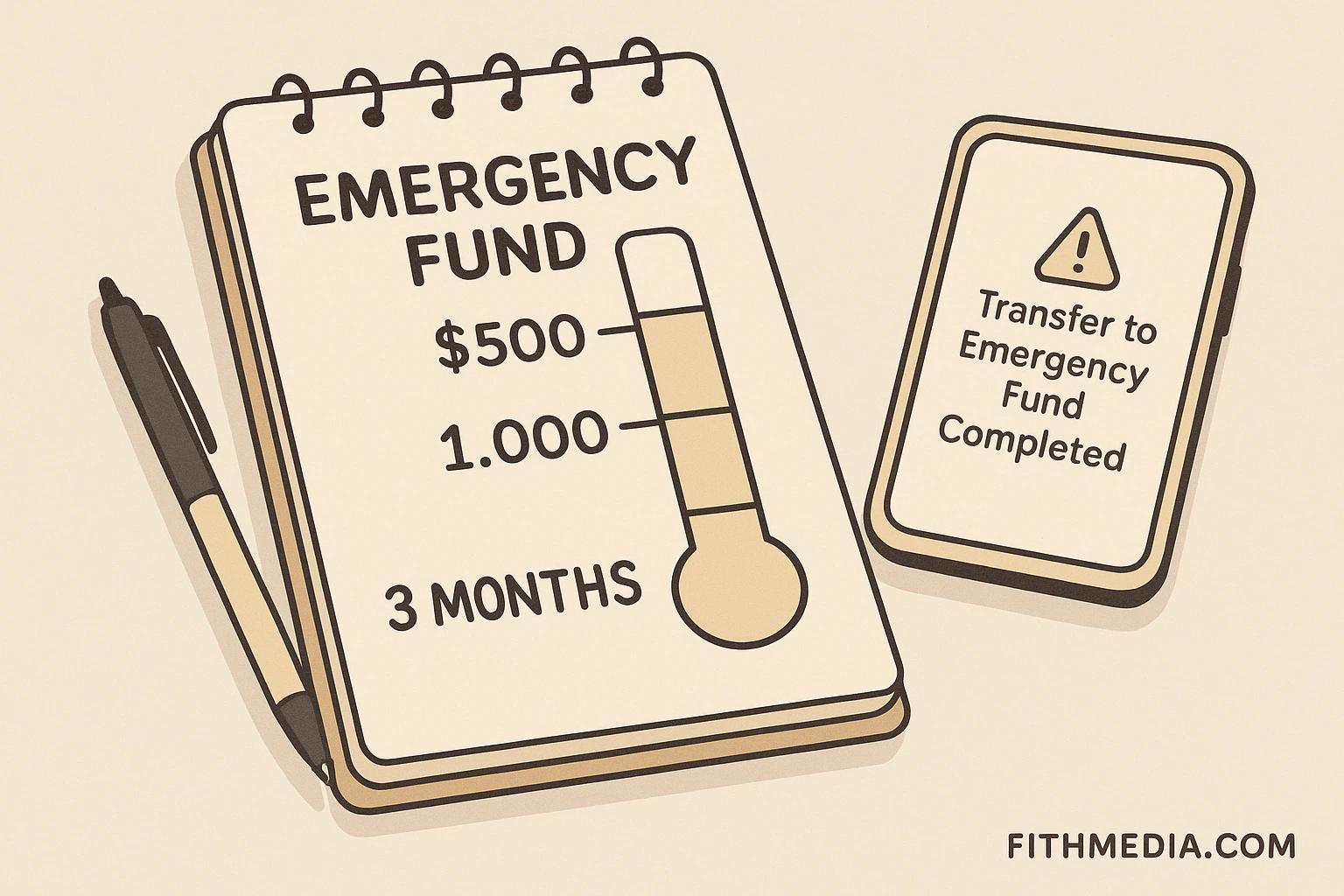

Tier 1: First $500 – The Fast Relief Fund

If you don’t have any savings yet, start with $500.

Why $500?

-

It’s reachable, even on a tight budget

-

It covers many small emergencies (tire blowout, co-pay, small repair)

-

It gives an immediate mental win and reduces anxiety

For many people, this is the point where they stop waking up worried about “what if something breaks?”

Tier 2: $1,000 – The Basic Safety Net

Next step: $1,000.

This level:

-

Handles bigger surprises (urgent dental work, car repair, travel)

-

Keeps many emergencies off your credit card

-

Gives breathing room between paycheck and panic

Think of it as your “Life Happens” buffer.

Tier 3: 1–3 Months of Expenses – Stability

Once you hit $1,000, your longer-term goal is 1–3 months of living expenses.

This is especially important if:

-

You are a renter

-

You have children

-

You work in a field where hours can get cut

-

You’re paying down debt and don’t want setbacks

This amount covers:

-

Rent / mortgage

-

Utilities

-

Groceries

-

Transportation

-

Minimum debt payments

-

Insurance

Enough to keep your life running while you figure out your next move.

Tier 4: 3–6 Months (or More) – Full Safety Net

A 3–6 month emergency fund is ideal for:

-

Freelancers and gig workers

-

Self-employed people

-

Single-income households

-

Anyone in a volatile industry (tech, hospitality, sales)

It’s not a hard rule, but a guideline. The more uncertain your income, the more months you should aim for.

Personalizing Your Goal (H3)

Ask yourself:

-

How stable is my job or main source of income?

-

Do I have kids or dependents relying on me?

-

Do I rent, own, or house-hack?

-

How quickly could I realistically find new work?

Your answers shape your emergency fund target. Don’t compare your number to someone else’s. Compare it to your reality.

Where Should You Keep Your Emergency Fund?

Your money needs a home that is:

-

Safe

-

Liquid (easy to access)

-

Separate from day-to-day spending

-

Earning at least some interest

Best Options in the USA

1. High-Yield Savings Account (HYSA)

-

Usually online banks

-

Higher interest rates than traditional savings

-

Easy transfers to checking

2. Money Market Account

-

Similar to savings but may require higher minimums

-

Often available at credit unions and online banks

3. Credit Union Savings

-

Community-focused

-

May offer competitive yields and flexible access

Places to Avoid for Your Emergency Fund

Don’t keep your emergency fund in:

-

Stocks → Value can drop the moment you need it

-

Crypto → Too volatile for safety money

-

Long-term CDs → Penalties if you withdraw too early

-

Under the mattress → No interest, higher risk

The emergency fund is not about growth. It’s about guaranteed availability.

Step-by-Step: How to Build an Emergency Fund from $0

This is where most people get stuck:

“How do I build an emergency fund when I feel broke already?”

Let’s break it down into simple, realistic steps.

Step 1: Know Your Bare-Minimum Monthly Number

You don’t need a perfect budget to get started. You just need a rough idea of:

-

Rent / mortgage

-

Utilities

-

Groceries

-

Transportation

-

Insurance

-

Minimum debt payments

Add those up. That’s your “survival number.”

It’s what your emergency fund is protecting.

Step 2: Choose Your First Goal

Pick one:

-

“My first goal is $250.”

-

“My first win is $500.”

-

“I want $1,000 by [month].”

Your brain needs something concrete and winnable.

Step 3: Automate Micro-Savings

Automation is the U.S. worker’s superpower.

You can set:

-

$5–$10 per day

-

Or $20–$50 per week

-

Or a percentage of your paycheck (e.g., 5%)

Use tools like:

-

Automatic transfers from checking to savings

-

Round-up apps (round up every transaction and save the spare change)

-

Employer direct deposit split (send part straight to savings)

Small, regular amounts beat “I’ll save what’s left” every time.

Step 4: Cut ONE Expense and Redirect It

You don’t need a full lifestyle overhaul. Start with just one thing.

Examples:

-

Cancel one unused streaming service → Save $15/month

-

Reduce takeout by once a week → Save $40–$60/month

-

Downgrade a phone plan or subscription box

Now redirect that exact amount to your emergency fund.

Turn “I cut this” into “I fund this.”

Step 5: Use Windfalls Wisely

Any extra money that appears should ask you a question first:

“Do you want more stuff… or more safety?”

Possible windfalls:

-

Tax refunds

-

Work bonus

-

Side hustle income

-

Cash gifts

-

Refunds and reimbursements

Try this rule:

-

At least 50% of any windfall goes straight to the emergency fund until you hit your first big goal.

Step 6: Protect Your Momentum

Momentum dies when:

-

You don’t see progress

-

You feel deprived

-

Your system is too complicated

So:

-

Track your balance weekly (not daily)

-

Celebrate milestones ($100, $250, $500, $1,000)

-

Use visual trackers (printable thermometer, habit app, wall chart)

Make this feel like building strength, not punishment.

The Psychology of an Emergency Fund: Why It Feels So Good

An emergency fund doesn’t just protect your money—it protects your mind.

How It Reduces Stress

When you know you can handle a surprise:

-

You sleep better

-

You argue less about money

-

You make calmer choices at work

-

You stop living in “what if” mode

Psychologists call it perceived control: feeling like you’re not helpless if something goes wrong.

How It Changes Behavior

People with emergency funds:

-

Swipe credit less often

-

Think more long-term

-

Feel safer taking smart risks (new job, starting a business)

It also makes other finance habits easier: budgeting, paying off debt, and investing feel less scary when you have a cushion.

Real-Life Scenarios: Emergency Fund USA in Action

Case 1: The Single Renter

Jordan, 28, lives in Chicago, rents a studio, works in marketing.

-

Sets a goal: $1,000 emergency fund

-

Uses auto-transfer: $50/week

-

Cancels 2 unused subscriptions (saves $25/month)

-

Adds half of a $600 tax refund

In 6 months, Jordan hits $1,100.

When their car needs $600 of repairs, they pay cash, no credit card, no panic.

The fund drops—but so does the anxiety. Then Jordan simply refills it using the same system.

Case 2: The Family with Kids

Maria and Devon have two children in Texas.

They aim for 3 months of expenses = $9,000.

-

Start with $500 fast using side gigs + selling unused items

-

Build to $2,000 over the year

-

Automate $150/month from joint checking

-

Put 70% of Devon’s annual bonus into the fund

After two years, they hit their full goal.

When Devon’s company downsizes and he’s between jobs for 2½ months, the family doesn’t miss rent or bills. They’re stressed about the situation—but not about losing their home.

Case 3: Freelance & Gig Worker

Kayla delivers for multiple apps and does freelance design. Income is inconsistent.

-

Aims for 6 months of “bare minimum” expenses

-

Tracks her lowest-earnings months and uses that as a baseline

-

Saves heavily in good months, but still a small amount in slow months

-

Keeps emergency fund in a HYSA separate from business funds

When two apps change their payout rules in the same month, she’s able to cover bills while adjusting her client mix. No payday loan. No panic swipe.

When Should You Actually Use Your Emergency Fund?

This is a big question—and a major search intent.

Use It When the Situation Is:

-

Unexpected – You didn’t see it coming

-

Necessary – You cannot reasonably avoid it

-

Urgent – It can’t wait until payday

Ask yourself:

“If I don’t pay this now, does something truly important break—work, health, home, or safety?”

If yes, your emergency fund is doing its job.

After You Use It: How to Refill

-

Pause extra debt payments temporarily

-

Rebuild the emergency fund back to your target

-

Resume your bigger goals once the cushion is restored

Think of it like:

Use → Refill → Resume.

Common Mistakes Americans Make with Emergency Funds

Avoid these traps:

-

Keeping it in checking → too easy to spend

-

Investing it all in stocks → can lose value right before you need it

-

Saving nothing because “it’s not enough” → small savings are still powerful

-

Using it for every inconvenience → it’s for real emergencies, not boredom

-

Not tracking progress → kills motivation

Remember: imperfect savings are still better than no safety net at all.

Systems & Automation: Make Your Safety Net Run Itself

Helpful Automations

-

Direct deposit split: employer sends part of paycheck straight to savings

-

Standing transfer: same day each week/month

-

Round-up apps: every purchase rounded up and saved

These tools are mobile-first and U.S.-friendly—great for readers on their phones.

Anti-Sabotage Moves

-

Turn off “view balance” widgets if they tempt you

-

Add a 24-hour rule before moving money out of your emergency fund

-

Keep the account at a different bank from your main checking (but still accessible within 1–2 days)

You don’t build a safety net all at once—you build it one rung at a time.

Recommended Links

Weave these naturally into the article:

-

Zero-Based Budgeting USA: Assign Every Dollar a Job

→ When you explain how to find savings to fund the emergency fund. -

Budgeting for Peace: Smart U.S. Money Habits That Last

→ When talking about emotional calm and budgeting as self-care. -

Financial Resilience 2026: Thrive Through Change

→ When you mention job loss, income shocks, or economic uncertainty. -

Buy Now Pay Later Risks 2026 USA: Fading Hype, Rising Debt

→ When explaining why an emergency fund is better than relying on BNPL or credit cards. -

The Quiet Millionaire 2026: U.S. Blueprint for Real Wealth

→ When discussing how calm, prepared households quietly build long-term wealth.

Conclusion: Your Safety Net Is a Love Letter to Your Future Self

An emergency fund is not just a financial product—it’s a promise you make to yourself and your loved ones. A promise that when life happens, you won’t have to panic, swipe, or borrow just to survive.

You don’t need to build it overnight.

You don’t need the “perfect” income.

You just need to start—with $10, $20, $50—and keep going.

Every dollar you place in that emergency fund is a quiet act of strength. It says:

“I’m planning for myself. I’m protecting my future. I’m giving myself time to think.”

In a country where money stress is loud and constant, your emergency fund is your silent shield.

Start where you are.

Protect what you have.

And let your financial safety net become the calm ground you stand on when life shakes.

Comment below with your questions or a win from your funds.

Like this article if the checklist helped.

Share it with a friend who needs a calm, practical plan right now.

Follow FithMedia for more guides on Finance, Tech, Health, and Lifestyle.

📣 Follow Our Social Media Pages

Stay in the loop with weekly tips, data-backed explainers, and simple templates you can use today:

Facebook · X (Twitter) · Instagram · Pinterest (search “FithMedia” and follow—your support helps us keep publishing high-quality, accessible finance content).

3 Comments