Zero-Based Budgeting USA: Assign Every Dollar a Job

November 18, 2025 · admin · Finance

If you’re searching for how Zero-Based Budgeting works in the USA, or you’ve heard the phrase “give every dollar a job” but aren’t sure how to make it practical for your life, you’re in the right place.

Across the country, Americans are rethinking how they budget. Rising prices, inconsistent income, and years of economic uncertainty have sparked a quiet financial shift. Many families no longer want complicated spreadsheets, strict budget rules, or guilt-driven systems that only work for a few weeks before collapsing.

People want a budget they can actually live with — a calm, clear plan that reduces stress, not increases it.

That’s why millions are adopting Zero-Based Budgeting, one of the simplest and most empowering systems in personal finance.

Zero-Based Budgeting (ZBB) gives every dollar a specific purpose before the month begins. Instead of guessing, hoping, or reacting, you take leadership over your money — calmly, intentionally, and with full control.

In this first part of our in-depth guide, we’ll explore:

-

What Zero-Based Budgeting really means

-

Why it works especially well for U.S. households

-

The psychological power behind “assigning every dollar”

-

Common misconceptions that hold people back

-

ZBB vs. traditional budgeting

-

The core principles of ZBB

-

The first four steps to setting up a ZBB plan

-

Real U.S. examples of families

-

Expert insights

Part 2 will go deeper into paycheck cycles, debt payoff, sinking funds, seasonal spending, long-term consistency, and advanced strategies.

For now, settle in. This system can transform your financial life — calmly, slowly, and without overwhelm.

What Zero-Based Budgeting Really Means

Zero-Based Budgeting is often misunderstood, so let’s simplify it.

Zero-Based Budgeting (ZBB) means that before the month begins, every dollar you expect to receive is assigned a purpose — until your “budget remainder” equals zero.

That does not mean you spend everything.

It means you give every dollar a job, such as:

-

Bills

-

Transportation

-

Groceries

-

Savings

-

Debt payments

-

Investing

-

Emergency fund

-

Sinking funds

-

Fun categories

-

Personal care

-

Giving

-

Subscriptions

-

House needs

If you earn $4,000 this month, you create a plan that allocates:

-

$4,000 on paper

-

$0 left “floating” or unassigned

Why?

Because unassigned dollars disappear.

This system creates clarity, order, intention — and peace.

Why Zero-Based Budgeting Works for U.S. Households

Americans today deal with a unique mix of:

-

High living costs

-

Subscription creep

-

Variable income

-

BNPL temptation

-

Rising credit card APRs

-

Unpredictable bills

-

Complex financial obligations

A Zero-Based Budget cuts through the noise by giving you:

1. A clear picture of where your money is going

No more guessing or anxiety around mid-month balances.

2. The ability to adapt to rising prices

When groceries go up, you adjust and reduce elsewhere.

3. Protection from lifestyle creep

Because every dollar already has a purpose.

4. A buffer against impulsive spending

Money without a job gets assigned to emotional impulses.

5. A better relationship with money

Many people report feeling calmer and more confident within the first month.

Zero-Based Budgeting is not strict. It’s not punitive.

It’s flexible, human, and deeply practical.

The Psychology Behind Zero-Based Budgeting (Why It Really Works)

Money is emotional — even when we pretend it isn’t.

Americans report feeling stress, anxiety, or guilt around budgeting. Zero-Based Budgeting helps because it rewires how your brain interacts with money.

1. It reduces decision fatigue

When every dollar already has a job, you make fewer choices throughout the month.

No more daily micro-decisions like:

-

“Can I afford this?”

-

“Should I get takeout?”

-

“Will my account be okay?”

Your budget already answered that.

2. It reduces impulsive spending

Having a spending plan reduces emotional purchases by up to 30%, according to behavioral finance research.

You’re no longer reacting to temptation; you’re following intention.

3. It creates a sense of control

ZBB gives psychological security because:

-

You know what’s coming

-

You know where money goes

-

You know what will get paid

-

You know how much is safe to spend

Clarity = calm.

4. It reassigns guilt to empowerment

A budget is not a punishment — it’s a plan.

This shift alone helps Americans feel more at peace with spending.

5. It builds confidence through small wins

Every time you stick to a category or save for a sinking fund, your brain gets a reward, increasing consistency.

Zero-Based Budgeting is not about perfection.

It’s about progress, one intentional month at a time.

🔍 Misconceptions About Zero-Based Budgeting (And the Truth)

Let’s clear up what Zero-Based Budgeting is not.

❌ Myth 1: “Zero-based budgeting means I can’t spend anything fun.”

✔ Truth: You should budget for fun — intentionally.

❌ Myth 2: “It’s too strict for real life.”

✔ Truth: ZBB is flexible. You can adjust mid-month when life changes.

❌ Myth 3: “I need a steady income or perfect paycheck timing.”

✔ Truth: It works for:

-

Salaried workers

-

Gig workers

-

Freelancers

-

Commission earners

You budget what you know, not what you hope.

❌ Myth 4: “If my budget hits zero, I’ll run out of money.”**

✔ Truth: Zero doesn’t mean “empty.”

It means everything is assigned.

❌ Myth 5: “It takes too long to start.”

✔ Truth: Your first month is the hardest.

Every month after becomes easier.

Zero-Based Budgeting vs. Traditional Budgeting

Understanding the difference helps you commit with confidence.

Traditional Budgeting

You:

-

List categories

-

Guess amounts

-

Hope to stay under

-

React to overspending

-

Move money around chaotically

It’s passive. It’s stressful.

Zero-Based Budgeting

You:

-

Know your income

-

Assign every dollar a job

-

Define your priorities

-

Adjust intentionally

-

Always know where you stand

It’s active. Empowering. Clear.

This is why ZBB has become one of the fastest-growing budgeting systems in the U.S.

Core Principles of Zero-Based Budgeting

These fundamentals guide everything you’ll do.

1. Income – Expenses = $0

Every dollar needs a job.

2. Give your dollars direction before the month begins

Planning ahead prevents emotional spending.

3. Every month is different

Budgets change with:

-

Season

-

Holidays

-

Bills

-

Weather

-

Travel

-

Income cycles

ZBB adapts.

4. You adjust, not abandon

If a category runs out, you adjust from another — intentionally.

5. Your budget should reflect your real life

It’s not meant to impress anyone.

It’s meant to serve you.

The Step-by-Step Zero-Based Budgeting Setup

This calm, simple structure works for any income level.

STEP 1 — Identify Your Monthly Income (What You Know for Sure)

This is your starting point.

Zero-Based Budgeting begins with the most predictable number you have:

Your take-home pay for the upcoming month.

Include:

-

Salary

-

Hourly wages

-

Freelance income you already earned or booked

-

Child support

-

Side income

-

Bonuses already confirmed

-

Social Security

-

Disability payments

-

Pension payments

Do not include:

-

“Hopeful” overtime

-

Possible tips

-

Hypothetical gigs

-

Expected but unconfirmed checks

ZBB is built on certainty, not optimism.

U.S. Example

Maria, a dental hygienist in Texas, earns:

-

$3,800 take-home pay

-

$400 predictable side income tutoring twice a month

Her ZBB income for next month = $4,200.

That’s her starting point.

STEP 2 — List Your True Monthly Expenses

These are your non-negotiables.

Think:

-

Rent/mortgage

-

Utilities

-

Groceries

-

Insurance

-

Debt payments

-

Transportation

-

Subscriptions

-

Internet

-

Childcare

Don’t guess — pull real numbers:

-

Bank statements

-

Receipts

-

Past bills

-

Email invoices

You want accuracy, not perfection.

U.S. Example

Using her bank statements, Maria identifies:

-

$1,400 → Rent

-

$160 → Car insurance

-

$210 → Groceries

-

$95 → Utilities

-

$65 → Phone bill

-

$115 → Gas

-

$200 → Student loan

-

$40 → Subscriptions

-

$60 → Internet

These become the first categories for her ZBB plan.

STEP 3 — Add Sinking Funds (Future-Proof Your Budget)

This is where ZBB shines.

Sinking funds help you save for predictable but non-monthly expenses:

-

Christmas

-

Birthdays

-

Car repairs

-

Back-to-school

-

Pets

-

Travel

-

Medical co-pays

-

House repairs

-

Clothing

-

Beauty and grooming

Instead of being surprised, you prepare gradually.

U.S. Example

Maria starts sinking funds:

-

Christmas → $50/month

-

Car maintenance → $40/month

-

Vacation fund → $75/month

-

Emergency fund → $100/month

Now her future bills won’t feel like emergencies.

STEP 4 — Add Lifestyle and Personal Choices

ZBB is not about deprivation.

You create categories for:

-

Eating out

-

Coffee shops

-

Hobbies

-

Self-care

-

Entertainment

-

Dating

-

Sports

-

Kids’ activities

A budget without joy is a diet — it won’t last.

U.S. Example

Maria allocates:

-

$120 → Eating out

-

$40 → Coffee

-

$50 → Hobbies

-

$30 → Personal care

Her budget now reflects her real life — not a fantasy she can’t sustain.

Where Part 1 Ends — and Where Part 2 Will Take You

By this point, you’ve:

-

Understood what Zero-Based Budgeting truly is

-

Learned why it works so well for American households

-

Seen the psychological power behind it

-

Cleared up common myths

-

Compared ZBB to traditional budgeting

-

Built your income foundation

-

Listed your essential expenses

-

Added sinking funds

-

Created lifestyle categories that fit your real life

In Part 2, we’ll go even deeper with the advanced half of Zero-Based Budgeting:

Now, in Part 2, you’ll:

-

Finish the ZBB setup

-

Learn how to run it paycheck by paycheck

-

See how to handle debt, savings, emergencies, and irregular income

-

Build monthly and quarterly rituals

-

Turn zero-based budgeting into a long-term, realistic rhythm for life in the U.S.

STEP 5 — Give Every Dollar a Job Until You Reach Zero

This is the heart of Zero-Based Budgeting.

You already know:

-

How much money is coming in

-

What your key expenses, sinking funds, and lifestyle needs are

Now you connect the two so that:

Income – All Assigned Dollars = 0

That doesn’t mean you spend every dollar.

It means every dollar has a job: save, spend, give, invest, protect, or pay down.

How to Do It in Practice

-

Start with your total monthly income at the top of your page or spreadsheet.

-

List your categories in this order (recommended, not rigid):

-

Housing

-

Utilities

-

Food

-

Transportation

-

Insurance

-

Debt payments

-

Subscriptions / utilities

-

Sinking funds

-

Savings / emergency fund

-

Fun / lifestyle

-

Giving or generosity

-

-

Assign amounts to each category based on your real expenses and goals.

-

After each assignment, subtract from the income total.

-

Keep going until your remainder is exactly $0.

Example: Simple U.S. ZBB Layout

Suppose your total monthly income is $4,200.

You might end up with something like:

-

Rent: $1,400

-

Utilities: $120

-

Internet: $60

-

Phone: $70

-

Groceries: $350

-

Gas/Transport: $200

-

Car insurance: $160

-

Health insurance (if separate): $200

-

Student loan: $200

-

Credit card minimums: $150

-

Subscriptions: $40

-

Emergency fund: $150

-

Christmas sinking fund: $50

-

Car maintenance sinking fund: $40

-

Vacation sinking fund: $75

-

Eating out: $150

-

Coffee / small treats: $40

-

Hobbies: $50

-

Personal care: $50

-

Kids’ activities: $100

-

Extra debt payment (beyond minimums): $200

-

Giving/Donations: $145

Total assigned = $4,200

Remainder = $0

Nothing is “just floating.” Everything has direction.

STEP 6 — Live the Budget: Track, Adjust, and Stay Kind to Yourself

Creating a zero-based budget is only half the story. The rest is learning to live with it in a gentle, sustainable way.

Tracking Doesn’t Have to Be Complicated

You have three main options:

-

Manual Tracking

-

Write spending in a notebook or simple spreadsheet

-

Update totals at the end of each day or every few days

-

-

App-Based Tracking

-

Use budgeting apps that support ZBB-style categories

-

Link accounts if you’re comfortable, or enter manually

-

-

Envelope or Digital Envelope Systems

-

More on this in a later section

-

Whatever method you choose, the goal is the same:

When you spend from a category, lower that category’s remaining amount.

That’s it. No perfection needed.

Adjust — Don’t Abandon

Real life rarely follows a blueprint perfectly.

-

Groceries might be higher one week

-

A small car repair might pop up

-

You might spend more on gas if you travel unexpectedly

Instead of labeling yourself “bad with money,” you practice the ZBB rule:

If one category goes over, adjust by reducing another category.

Examples:

-

Groceries went $40 over? Cut $40 from eating out this month.

-

Extra gas this month? Trim from hobbies or a non-urgent sinking fund.

This keeps the budget total balanced without guilt.

Use Weekly Check-Ins

Instead of waiting until the month ends, schedule:

-

10–20 minutes once a week

-

Quick review:

-

What did I spend?

-

Which categories are low or high?

-

What can I adjust now, while there’s still time?

-

Think of it as a calm “money meeting” with yourself or your household.

STEP 7 — Build a Paycheck-Based Zero-Based Budget

Most Americans don’t think in “monthly income.”

They think in paychecks.

-

Every 2 weeks

-

Twice a month

-

Weekly

-

Monthly

-

Or irregular (for gig workers and freelancers)

Zero-Based Budgeting works best when you adapt it to how your money actually arrives.

Paycheck Budgeting for Bi-Weekly Pay (Every 2 Weeks)

If you get paid every two weeks, you usually receive:

-

26 paychecks per year

-

Most months: 2 paychecks

-

A few months: 3 paychecks

How to Use ZBB Bi-Weekly

-

Start with your monthly ZBB plan (from Steps 1–5).

-

Divide bills and categories by pay period.

For example:

-

Paycheck 1 (early month) covers:

-

Rent

-

Utilities

-

Internet

-

Some groceries

-

Sinking funds

-

-

Paycheck 2 (mid-month) covers:

-

Debt payments

-

Groceries

-

Gas

-

Lifestyle spending

-

Rest of sinking funds

-

You assign every dollar of each paycheck a job before it arrives.

Semi-Monthly Pay (e.g., 1st and 15th)

Some employers pay on set dates:

-

1st and 15th

-

15th and 30th

This actually pairs nicely with “monthly” thinking.

You:

-

Plan the full month

-

Decide which half of the month’s bills each paycheck covers

-

Ensure that big items (like rent) have a clear place

One paycheck may focus heavily on housing, the other on debt and food.

Weekly Paycheck ZBB

If you’re paid weekly, your ZBB might be more granular:

-

Paycheck 1: Rent portion + gas + a week of groceries

-

Paycheck 2: Utilities + subscriptions + a week of groceries + sinking funds

-

Paycheck 3: Debt payments + groceries + gas

-

Paycheck 4: Savings + any remaining monthly categories

Some people used to weekly pay prefer a “four-week budget” instead of a calendar month. Either way can work — ZBB is flexible.

Handling Irregular or Gig Income with ZBB

This is where many Americans get stuck. But ZBB can absolutely work for:

-

Uber/Lyft drivers

-

Doordash or Instacart workers

-

Freelancers and contractors

-

Tip-based workers

-

Commission-based sales roles

Here’s a simple approach:

1. Use a “Baseline Budget”

Calculate your bare minimum monthly needs:

-

Rent, utilities, food, transportation, minimum debt payments, insurance

This is your Survival Budget — what you absolutely must cover.

2. Use a Rolling Income Average

Look at the last 3–6 months:

-

Total your net income

-

Divide by the number of months

-

That average = planned baseline income

You build your ZBB plan off this average, not your best month.

3. Use Income Buckets

When you get paid:

-

First, fund your Survival Budget for the upcoming period

-

Second, fund sinking funds and savings

-

Third, fund extra debt payments and lifestyle

If you have a great month, the extra doesn’t vanish — it goes to:

-

Emergency fund

-

Sinking funds

-

Extra debt payments

In lean months, you rely on:

-

The surplus you built during stronger months

This keeps your ZBB rooted in reality instead of hopes.

STEP 8 — Integrate Debt Payoff into Zero-Based Budgeting

Debt is a major stress source for U.S. households. ZBB helps you tackle it without losing your mind.

Start with Minimums

-

Include minimum payments for all debts in your core budget:

-

Credit cards

-

Student loans

-

Personal loans

-

Auto loans

-

Medical debt

-

Then Assign Extra

-

Decide how much extra you can assign to debt each month after covering essentials and modest sinking funds.

This “extra” might be:

-

$50

-

$100

-

$200

-

More, if your budget allows

ZBB makes this number crystal clear: you see exactly how much you can afford to put toward debt each month without guessing.

Debt Snowball vs Debt Avalanche

ZBB plays well with both strategies.

Debt Snowball

-

Pay extra on the smallest balance first

-

Once it’s gone, roll that payment onto the next smallest

-

Emotionally motivating — lots of quick wins

Debt Avalanche

-

Pay extra on the highest interest rate first

-

Mathematically fastest way to pay least interest

-

Progress may feel slower emotionally

ZBB doesn’t force you to choose one. You can:

-

Start with snowball to build momentum

-

Switch to avalanche when you feel stronger

-

Or blend both (e.g., pay off one small card, then attack a high-rate loan)

Example: Debt + ZBB in Action

Say you have:

-

$4,200 income

-

$3,500 total assigned to essential categories, sinking funds, basics

You have $700 left to assign a job.

You could:

-

Put $400 toward extra debt payments

-

Put $200 into emergency fund

-

Put $100 toward a savings or investment category

Your ZBB forces you to decide intentionally how much goes where — instead of letting leftover money drift.

STEP 9 — Build an Emergency Fund Using Zero-Based Budgeting

Your emergency fund is your financial safety net — and ZBB is one of the best tools for building it.

Define Your Emergency Fund Ladder

You might set targets like:

-

Step 1: $500

-

Step 2: $1,000

-

Step 3: One month of expenses

-

Step 4: Three months of expenses

Within your ZBB categories, you choose:

-

“Emergency Fund – First $500”

-

Later, “Emergency Fund – $1,000 Goal”

Then assign:

-

A specific monthly amount (e.g., $50, $100, $200+)

Because ZBB sees every dollar, you know:

-

Exactly how much you’re contributing

-

Exactly where it can come from

-

Exactly how long it may take to reach your milestone

Over time, your emergency fund becomes a core non-negotiable category, just like rent or groceries.

STEP 10 — Use Advanced Sinking Funds and Seasonal Planning

Once your basic ZBB system is stable, you can get more nuanced with sinking funds.

What Are Advanced Sinking Funds?

Beyond Christmas and car repairs, you might add:

-

Annual insurance premiums

-

Professional license renewals

-

Kids’ sports seasons

-

Back-to-school expenses

-

Pet vet visits

-

Home appliance replacement fund

-

Yearly technology upgrades (phone, laptop)

-

Planned travel, conferences, or retreats

Each becomes its own line in your budget.

Seasonal ZBB in the USA

American spending often follows patterns:

-

January–February: Holidays are over, fresh-start energy, sometimes carrying December costs

-

Spring: Tax refunds, travel planning, school activities

-

Summer: Camps, vacations, higher utility bills

-

Fall: Back-to-school, sports, holidays approaching

-

Winter: Holiday spending, heating, gatherings

A seasoned zero-based budgeter learns to:

-

Look at the upcoming 2–3 months

-

Add sinking funds accordingly

-

Increase or decrease certain categories seasonally

This helps you avoid the “every year this surprises me” loop.

Cash Envelopes vs Digital Envelopes: Which Fits You?

Zero-based budgeting pairs well with the idea of envelopes, where each category has a visual limit.

Cash Envelopes

You:

-

Withdraw cash

-

Place it in labeled envelopes (Groceries, Eating Out, Gas, Fun, etc.)

-

Spend only what’s in each envelope

Pros:

-

Very tangible

-

Hard to overspend

-

Great for impulse control

Cons:

-

Less convenient in a digital world

-

May feel unsafe or cumbersome for some

Digital Envelopes

You:

-

Use a budgeting app or bank tools

-

Assign digital “envelopes” or categories

-

Track spending against them

Pros:

-

Mobile-friendly

-

Bank-linked

-

Easy to adjust

-

Great for online purchases

Cons:

-

Requires you to stay engaged with the app

-

Not as physically “real” as cash for some people

You can even blend both:

-

Use cash envelopes for one or two problem areas (e.g., eating out, entertainment)

-

Use digital tracking for everything else

ZBB doesn’t dictate the medium. It just requires that each dollar belongs somewhere.

Monthly and Quarterly Zero-Based Budget Rituals

Long-term success with ZBB depends on rhythm, not willpower.

Monthly Ritual (End of Month / Start of Month)

-

Review last month:

-

Where did you overspend?

-

Where did you underspend?

-

What surprised you?

-

-

Tweak categories:

-

Adjust amounts realistically

-

Add/remove categories as life changes

-

-

Reset for the new month:

-

Update income

-

Recalculate sinking fund contributions

-

Confirm debt and savings targets

-

-

Clarify one focus:

-

“This month I will focus on reducing impulse buys”

-

Or: “This month I will grow my emergency fund by $200”

-

Quarterly Ritual (Every 3 Months)

-

Review all subscriptions and recurring bills

-

Evaluate sinking fund progress

-

Check how much you’ve paid toward debt

-

Look at emergency fund growth

-

Adjust your long-term targets:

-

Increase savings percentage

-

Shift categories based on life events

-

These rituals make ZBB feel like care, not control.

Real-Life U.S. Stories: Zero-Based Budgeting Over Time

Case 1: The Overwhelmed Teacher

Kara, a middle-school teacher, felt like money was constantly “disappearing.” She:

-

Started ZBB with $3,600 monthly income

-

Realized she was spending $300+ on random food and subscription creep

-

Reassigned that money:

-

$150 → Emergency fund

-

$100 → Extra debt

-

$50 → Sinking funds

-

After 9 months:

-

Paid off one credit card completely

-

Built a $1,200 emergency fund

-

Reported less money anxiety, especially before payday

Case 2: The Young Couple with Debt

Evan and Jasmine:

-

Combined take-home: $6,200/month

-

Student loans, car loan, credit cards

With ZBB, they:

-

Put every dollar into categories

-

Set a goal: $600/month extra to debt

-

Used the debt snowball with their smallest card first

18 months later:

-

Paid off 3 credit cards

-

Redirected snowball money toward student loans

-

Began saving for a home down payment

They didn’t get a huge raise.

They simply gave their dollars better jobs.

Case 3: The Freelance Designer

Leo, a freelance designer in California:

-

Inconsistent income

-

Often panicked during slow months

With ZBB plus income buckets:

-

Set a baseline Survivor Budget of $2,500

-

Averaged last 6 months of income at $3,200

-

Built a “Business Buffer” sinking fund with good months

Result:

-

Slow months no longer felt like collapse

-

Could still fund essentials and a little savings

-

Used extra “good month” income to pay down a personal loan

ZBB didn’t make income stable — it made Leo’s response to it stable.

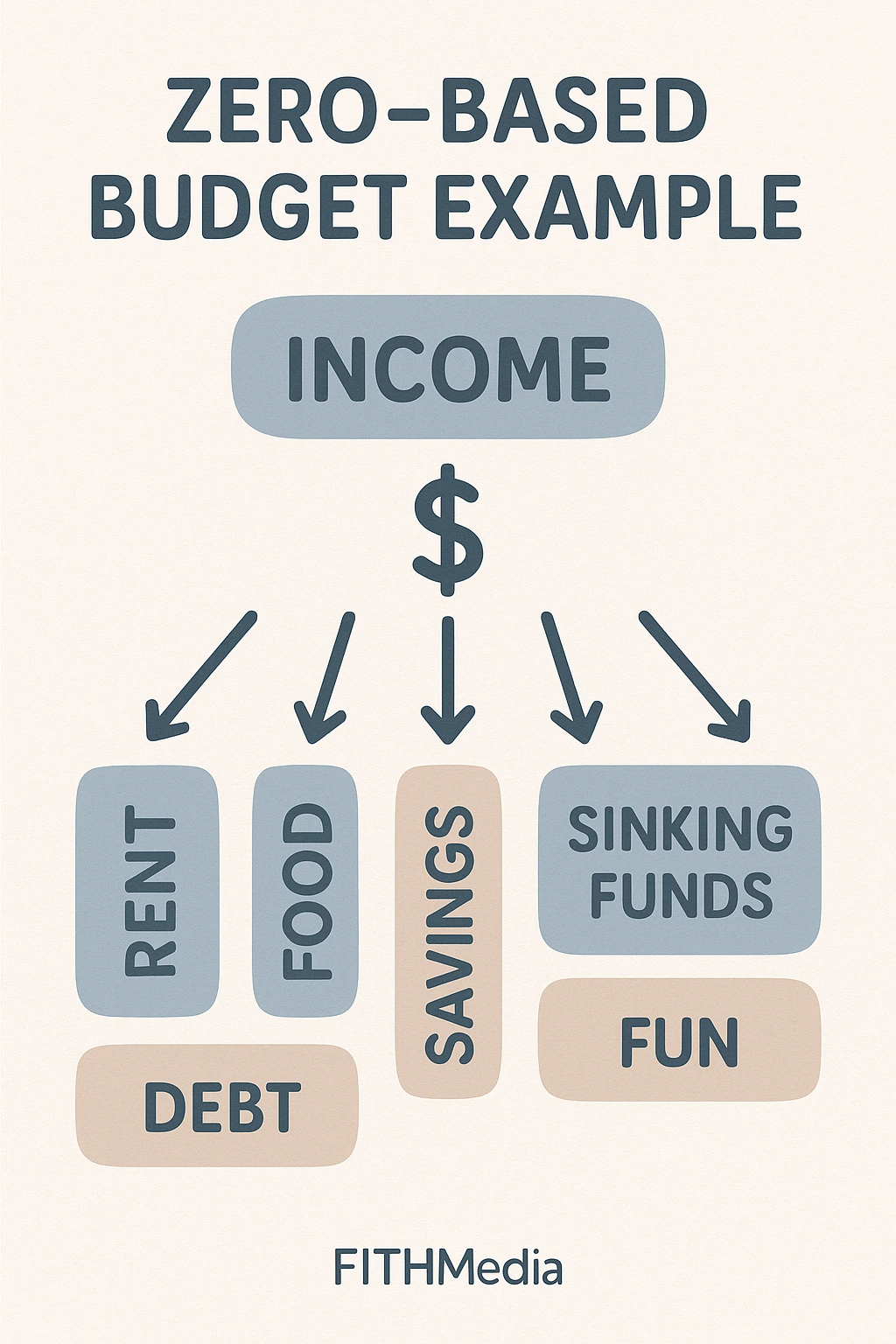

A simple zero-based budget example showing how every dollar of income is assigned to a specific category.

Recommended Suggestions

-

“Budgeting for Peace: Smart U.S. Money Habits That Last”

→ When talking about the emotional benefits and calm mindset -

“Emergency Fund USA: Build Your Financial Safety Net”

→ When explaining how ZBB helps you grow an emergency fund -

“Subscription Audit USA: Cut Hidden Monthly Fees”

→ When covering subscription categories and freeing money -

“Financial Resilience 2026: U.S. Guide to Thrive Through Change”

→ When exploring economic uncertainty and adaptability -

“The Quiet Millionaire Movement in 2026”

→ When you discuss long-term wealth built quietly through discipline

Conclusion: Zero-Based Budgeting as a Calm Financial Rhythm

Zero-Based Budgeting isn’t a trend.

It’s a way of thinking about money that:

-

Reduces guesswork

-

Increases clarity

-

Honors your real life

-

Respects your emotions

-

Protects your future

By giving every dollar a job, you trade:

-

Chaos for clarity

-

Anxiety for awareness

-

Reaction for intention

-

“Where did my money go?” for “I know where every dollar is.”

It doesn’t matter if your income is large or small, steady or irregular.

Zero-Based Budgeting meets you where you are and helps you direct what you have.

You don’t need to get it perfect this month.

Or next month.

Or ever.

You only need to:

-

Keep planning

-

Keep assigning

-

Keep adjusting

-

Keep learning from your own numbers

Over time, your budget stops being a punishment and becomes a quiet, loyal assistant — a monthly reflection of your values and priorities.

And that’s the real power of Zero-Based Budgeting USA:

Not just more control over money, but more peace in how you live with it.

Comment below with your questions or a win from your budget.

Like this article if the checklist helped.

Share it with a friend who needs a calm, practical plan right now.

Follow FithMedia for more guides on Finance, Tech, Health, and Lifestyle.

📣 Follow Our Social Media Pages

Stay in the loop with weekly tips, data-backed explainers, and simple templates you can use today:

Facebook · X (Twitter) · Instagram · Pinterest (search “FithMedia” and follow—your support helps us keep publishing high-quality, accessible finance content).

4 Comments